It's a common question: does student loan debt go away when you die? And in a world of uncertainty, there are only a few things you can be certain of: Death, taxes….and student loans.

Unfortunately, student loans are one of the most difficult types of debt to discharge, and in some cases, they can follow you beyond the grave. Now, most loans are discharged at death, but not always.

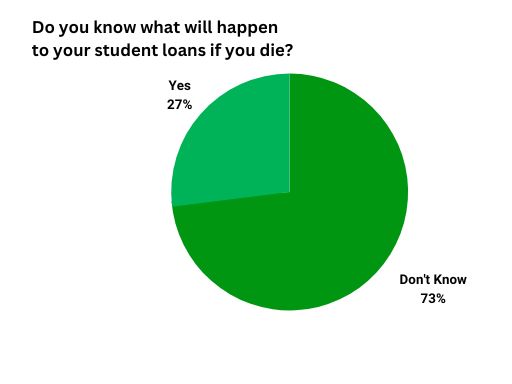

And the sad reality is that 73% of borrowers have no idea what happens to student loans when you die (according to a survey by Haven Life).

So let’s change that statistic, shall we?

If you have federal or private student loans, or are a co-signer on either, it’s important to have a plan in place in case of an untimely death. In this article, we’ll uncover the truth about student loans after death, and review the details of each type of student loan to show who is responsible for this debt after death.

Key Points

- The death of a student loan borrower doesn't always mean that their loans are automatically forgiven.

- Federal loan discharge balances on student loans when you die (including Parent PLUS loans).

- Private student loans, on the other hand, do not necessarily get discharged upon the borrower's death. The policies regarding death discharge vary by lender, and borrowers are advised to review their loan agreements to understand their options.

- If a borrower has a co-signer on their private student loan, the co-signer may be responsible for the debt after the borrower's death, depending on the lender's policies.

- Borrowers should review the terms of their loans and consider purchasing life insurance policies to repay their debts in the event of their death.

- Tips for borrowers to manage student loan debt during their lifetime include taking advantage of loan forgiveness programs, refinancing to a lower interest rate, and seeking the help of a financial advisor or credit counselor.

“I am a retired teacher who is still paying off loans for my Masters degree and at the same time the older of my two children has begun accruing her own student loans and the younger child will be headed to college and getting those loans in another year and a half. I foresee helping pay these down until I die...death, taxes, and student loans are now inevitable.”

– K, El Paso TX

What happens to federal student loans when you die?

Federal student loan debt is discharged in the event of death of the borrower. This means that no one is responsible for your federal student loans if you die; Not your spouse, not your parents, and not your children.

Proof of death is typically required to get the deceased's federal student loans canceled. So you must present the lender with an original death certificate, a certified copy of the death certificate, or an accurate and complete photocopy of one of those documents.

What happens to Parent PLUS loans upon death?

Parent PLUS loans are federal student loans borrowed by the parent(s) of a child undergraduate student. These loans are the responsibility of the parent.

Parent PLUS loans are also discharged in the event of death of the student or the parent (borrower). And due to the passing of the Tax Cuts and Jobs Act of 2017, loan discharges starting in 2018 are not considered taxable income.

And it’s important to note that Parent PLUS loans only allow one borrower, so if one parent dies (and they are not the Parent PLUS loan borrower), the surviving parent is still responsible for the loan balance.

What happens to PLUS loan endorsers?

If there is an “endorser” (co-borrower) on a PLUS loan, the endorser is equally responsible for repaying the loan if the primary borrower falls behind on payments.

But if either the student or the primary borrower dies, the PLUS loans are discharged and the endorser is no longer obligated to repay the loan. This applies to both Grad PLUS and Parent PLUS loan endorsers.

What happens to private student loans when you die?

Private student loans are loans from private lenders (i.e. not “Direct Loans”) that have different rules around loan forgiveness and discharge.

These may or may not be discharged in the event of death of the borrower.

And if you have no cosigner, the borrower may come for your estate to collect the debt after your death.

Those with private student loan debt should contact their borrower to learn about their death discharge policy.

There are several popular private student loan companies that may offer loan discharge if you die, including:

Requirements for loan discharge will vary from lender to lender, so make sure to review your loan documents, or talk to your lender directly to understand what is required to complete the loan discharge.

What happens to parent private student loans upon death?

If you are a parent that has private student loans for your child, you may be eligible for forgiveness of these loans if you or your child dies…but not always. Each lender has their own policies for loan discharge, and parents may still be responsible for student loans, even if the child dies.

For your specific loan policies on loan discharge after death, please contact your lender to learn more.

What happens to co-signed private student loans upon death?

A cosigner is liable for your student loan debt if you fall behind or default on your payments. If you pass away, your loan co-signer may still be on the hook for your private student debts, depending on the lending institution.

Policies around cosigners vary by lender, and you should review your loan documentation for exactly how they handle co-signed loans.

Luckily, the Economic Growth, Regulatory Relief and Consumer Protection Act now requires private lenders to release cosigners from student loan debt obligations if the student dies, but this only applies to loans made after Nov. 20, 2018. For loans that originated before then, it is still up to the lender’s discretion.

How to protect your family financially in case of a death

Death and student loans can be complicated, and if you find yourself holding a loan that still requires payment after death, there are a few steps you can take to protect yourself and your family financially:

#1 Review your loan policy

It’s important to know the exact policy details of how your lender handles death - and what steps to take to complete the discharge process.

If you have federal loans, you can log into your student loan account on StudentAid.gov to find your loans and loan servicer information.

If you have private student loan debt, log into your lender’s website and download a copy of your loan agreement and policies. If you can’t find it, call your lender and have them email or mail you a copy.

Review the private loan policies to see how they handle death, including how it affects your spouse, parents, and co-signers (if applicable).

Keep a copy of the requirements and contact information of your lender in the case of death so that loved ones can quickly and easily take care of the student loan discharge process in the event of your death.

#2 Get a life insurance policy

If you still have student loan debt, protecting your family from inheriting those debts in case of death is important. As they might get passed on after your death to your family (or a co-signer), you must consider having a life insurance policy to help pay off the loans.

And if you are the parent or spouse of someone that is a student borrower with a private student loan that you are liable for, you should consider pulling out a life insurance policy on the borrower.

Term life insurance policies are a simple way to get low-cost life insurance with enough coverage to take care of outstanding debts and financial obligations.

Be sure to shop around for competitive rates and consider different types of policies such as term life insurance policies or whole life policies.

#3 Consider refinancing your private student loans

For more immediate protection, you can also consider refinancing private student loans, especially if your current lender does not offer immediate discharge of loans due to death.

Refinancing can also help you consolidate multiple loans into one, allowing you to work with only a single lender, instead of multiple lenders that may come after your family or estate after death.

If you decide to refinance your student loans, shop around and compare lender reviews (like this one of Earnest or SoFi, both very popular lenders). Above all else, read the fine print to learn how the offering fits your situation.

Frequently asked questions

How to notify a servicer in the event of a death?

To contact your student loan servicer, it is best to call them, or send an email to the customer service team. For federal loans, you can call the Federal Student Aid Information Center at (800) 433-3243. For private loans, you will need to look up the lender and find their contact information on their website.

Once you get a hold of the loan servicer, they can walk you through the requirements to complete the loan discharge.

Are there taxes on discharged student loans?

Prior to 2018, student loans that were discharged due to death or permanent disability were considered taxable income. But with the passing of the Tax Cuts and Jobs Act of 2017, loans discharged due to death or disability are no longer taxable.

This tax-free provision is set to expire at the end of 2025.

Can you inherit student loan debt?

In general, no, you can’t inherit student loan debt. This means that children of student loan borrowers will not be on the hook for loans if their parent dies, and the same goes for spouses, or next of kin.

The only exception is if you are a co-signer on a private student loan before Nov. 20, 2018, some private lenders may still require repayment, even if the primary borrower dies. Federal law now prevents this (on loans made after Nov. 20, 2018), automatically waiving the debt for co-signers if the primary borrower dies.

Is my spouse responsible for my student loans if I die?

If your spouse passes away with student loan debt, in certain states you could be responsible — because student loans are considered community property in some states.

If your spouse takes out student loans while you are married, and you live in a community property state (such as Arizona or Texas), you may be liable for those loans if your spouse dies. Student loans are considered community property when taken out during a marriage, and follow the state laws that assign repayment responsibility to both spouses.

What happens if you marry someone with student loans?

If you marry someone that already has student loans, you are not responsible for the repayment of those loans if your spouse dies. Even in community property states, if the loans originated before you were married, they are considered separate property, and are only the responsibility of the borrower.

Do student loans go away after 7 years?

No. Student loans stay with you for life, and require full repayment, or to qualify for some type of loan forgiveness. And there is no loan forgiveness program that gets rid of student loans in just seven years.

Now, student loans defaults are reported to the major credit bureaus, and can be removed from your credit report after seven years of good standing. But just because the default status or late payment report is removed from your credit history, this does not remove your responsibility to repay your loans in full.

Should I remove co-signers?

Removing co-signers from your student loans can help remove the burden of repayment from your co-signer, and possibly even increase their credit score. As a co-signer, your student loan debt will increase their debt-to-income ratio (DTI), which can negatively reflect in their credit score.

To remove a co-signer from your loans, there are a few options:

- Apply for co-signer release. Most lenders allow you to release a co-signer after a certain number of on-time payments. You may need to undergo a full credit review and have to provide income statements and other financial information to be approved.

- Refinance. You can remove a co-signer by refinancing your student loans, as long as you can qualify for a refinance on your own. If your income and credit profile have improved since you first applied for a student loan, you may be able to qualify for a refinance. There are no timeline requirements for refinancing, you can do this at any time.