If you have an emergency expense and not enough funds in your bank account, a cash advance can cover the difference. Unfortunately, many people use credit card cash advances and payday loans to get extra funds. Those common choices result in high-interest rates and future obstacles, but there is a better way to get money when you need it.

Cash advance apps like Albert let you borrow hundreds of dollars at 0% APR. Some of these apps have affordable membership plans, while others let you access the money without making any type of payment. These apps can keep you away from credit card debt and payday loans, but which cash advance apps are the best?

This article will cover what makes the Albert cash advance app uniquw and compare it with some of the other top choices. You will learn about cash advance apps, online banking apps, employer-sponsored apps, and peer-to-peer apps that can give you extra funds when you need them. Reviewing several apps is important so you get paired with the right one for your financial needs.

How Apps Like Albert Work

Cash advance apps like Albert connect to your bank account and provide extra funds when you need them. You don’t pay any interest on the cash advance, and you won’t get penalized for having a bad credit score. These apps do not conduct credit checks which makes it easier to qualify. Cash advance apps look at your banking activity to determine your maximum cash advance. Albert and other apps then use your incoming funds to repay the cash advance.

About Albert

Albert is a financial app that helps users bank, save, and invest. Users can request a cash advance of up to $250 without any APR. This cash advance can help you avoid overdrafts which can save hundreds of dollars each year. Albert lets you automate your savings and investments based on your income, spending, and bills. When you invest, you don’t need much to get started. Albert users can buy fractional shares for as little as $1. The bank accounts on Albert’s platform are insured by the FDIC.

Key Features

- Cash advances up to $250

- No interest

- Instant transfers for a small fee or 2-3 days for free

- 4.6 of 5 stars on the App Store with ~150,000 reviews

Pros

- Get quick access to cash: You can instantly get up to $250, depending on your deposit activity. Albert users can also wait 2-3 business days to receive cash and avoid a fee in the process.

- 0% APR: You don’t have to worry about a high interest rate dragging you deeper into debt. The $250 cash advance does not come with the high fees and APR you can expect from a credit card cash advance.

- No credit check: Obtaining a cash advance from Albert will not hurt your credit score. Since Albert does not conduct a credit check, you can borrow money even if you don’t have the best credit score.

Cons

- You can only borrow up to $250: If you need to borrow more than $250 for your emergency expenses or anything else, you will need to get additional funds from somewhere else.

- Albert does not improve your credit score: A cash advance technically is not a loan, and that means paying it off will not help your credit score.

- Repayment happens automatically: While the automatic repayment policy can reduce stress, it can also become inconvenient. Some cash advance app users get trapped in a cycle of requesting cash advances to cover emergency costs. Even if you get caught up in a short-term cash advance cycle, you will likely save money compared to a payday loan or credit card cash advance.

Is Albert Different Than Other Cash Advance Apps?

Albert isn’t just a cash advance app. The company offers a suite of financial products and services, such as bank accounts and investment portfolios. You can buy stocks on Albert and build up to key savings goals. Albert tracks bills and shares some suggestions on how to save money.

8 Apps Like Albert

Albert is a useful cash advance app that has won the trust of over 10 million members. However, some members may seek alternatives, and if you’re new to cash advance apps, it’s a good idea to know your options. These cash advance apps also deliver exceptional services for their users.

Dave: Best for Career Growth

Dave is a mobile banking app that lets users take out cash advances of up to $500. The fintech platform was launched in 2019 and has over 12 million users. The app’s success has attracted many investors, such as Mark Cuban and Corbin Capital Partners.

Highlights

Pros

- Higher cash advance than most apps: Dave lets you borrow up to $500 for a cash advance. Most cash advance apps set a $200-$300 limit that depends on your bank account’s activity.

- Discover side hustles and job opportunities: Dave has a section in its app dedicated to side hustles. If you want to earn some extra cash, Dave can connect you with opportunities.

- Avoid overdraft fees: A cash advance from Dave can save you from pesky overdraft fees. Those fees can quickly add up at traditional banks.

Cons

- You have to pay $1/mo to use the app: You can get a higher cash advance at 0% APR with Dave, but it will cost you. The $1/mo subscription is manageable and can be worth it, but the subscription is not for everyone.

- You can pay up to $13.99 for an instant transfer: Dave has different fees depending on whether you send the funds to an internal or external account. You can also expect a higher fee if you request more funds. Other cash advance apps have lower fees for each request.

- Dave has an auto repayment system: Just like Albert, this is a pro that can become a con. Automatic repayments remove stress, and other methods of obtaining funds may result in late fees. However, Dave can pull money from your bank account even if you aren’t prepared.

Cleo: Best for Building Credit

Cleo is a cash advance app that lets members borrow up to $250. The app has savings features that let you allocate funds to goal-based accounts. These accounts can strengthen your finances and help you get more intentional with every dollar you earn. Cleo also has a Credit Builder Card you can use to improve your credit score with every purchase and on-time payment.

Highlights

Pros

- No credit check: Cleo does not conduct credit checks or look at your credit score when giving out cash advances.

- Improve your credit: Paying back a cash advance will not improve your score. However, Cleo lets members get a Credit Card Builder, which is the company’s version of a secured credit card.

- Allocate funds across multiple savings accounts: You can distribute your paycheck based on your goals. Want to save for a vacation, emergency fund, and down payment? Cleo streamlines the process.

Cons

- Low cash advance: Cleo only lets you borrow up to $250, but you will start off with a lower limit between $20 and $70. If you need more money to cover emergency expenses, you may have to use another app.

- Standard fee for Express Transfers: While a standard fee indicates how much you will pay every time, $3.99 can feel a bit high if you don’t need much money. Whether you borrow $25 or $250, you will have to pay the $3.99 fee for an Express Transfer.

- No FDIC insurance: Cleo Wallet does not have backing from a federally insured bank. The funds in your account will not earn interest, and if the bank goes under, you won’t get your money back. The Cleo Credit Builder Card is issued by WebBank, which is a member of the FDIC.

Online Banking Apps Like Albert

Albert connects their members with mobile banking solutions that go beyond a cash advance to help with emergency expenses. Here are some online banking apps like Albert to consider.

Varo: Best for High APY Savings Accounts

Varo is a mobile banking app with high-interest savings accounts, $250 cash advances, and other perks. Qualifying Varo members can earn up to 5% APY on their savings, which is more than most CDs. You can access funds from your Varo savings account at any time and watch as your account grows each month. The company also offers debit cards and secured credit cards.

Highlights

Pros

- More flexible repayment terms: You can repay a Varo cash advance within 30 days. Most cash advance apps automatically take funds out of your account on your next payday.

- High interest rate on a savings account: The minimum interest rate is 3% APY which is already respectable. However, if you make enough purchases on your Varo debit card and continue depositing funds into your account, you can qualify for a 5% APY.

- You can get a secured credit card: Varo offers secured credit cards for people who need to build credit. A higher credit score can help you score a lower interest rate on a mortgage, auto loan, personal loan, and similar financial products.

Cons

- High fees on the cash advance: You have to pay a $15 fee to access a $250 cash advance. The fee is lower if you borrow less money, but you’re looking at a $4 fee or higher if you borrow more than $20. That’s not ideal compared to the other choices.

- 3% APY on any balance over $5,000: The enticing 5% APY is only in effect for the first $5,000 in your Varo savings account. Any dollar above $5,000 grows at 3% APY. It’s still higher than most savings rates, but you might be able to earn more on a CD.

- No physical branches: If you use mobile banking, you’re bound to run into this issue. Mobile banking apps have solutions for accessing physical cash, speaking with a representative, and depositing checks. Some people prefer physical branches, but these apps make the adjustment to no physical branches seamless.

MoneyLion: Best for Personalization

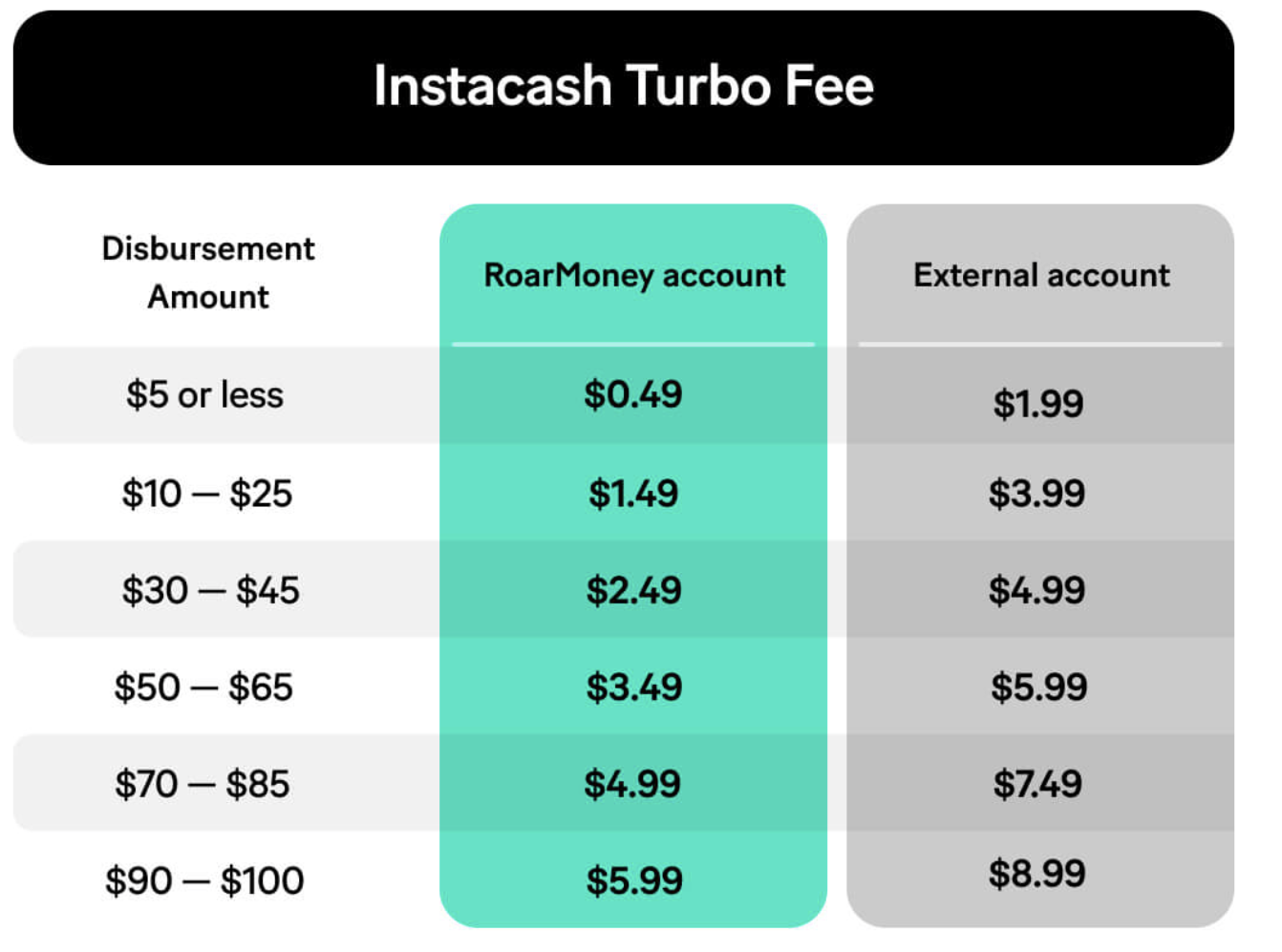

MoneyLion is a mobile banking app that lets users borrow up to $500 through Instacash. The cash advance does not come with monthly fees or interest. You only get charged a fee if you request an instant transfer. MoneyLion has a table that shows how much you will have to pay.

MoneyLion lets you access up to $700 if you join the Credit Builder Plus program. RoarMoney members can take out a $1,000 cash advance. Your cash advance limit depends on your banking activity. Every member starts with a maximum $10 cash advance that grows as you make consistent monthly deposits into your account.

Highlights

Pros

- Higher cash advance than most apps: MoneyLion recently increased its cash advance from $250 to $500. You can also borrow $700 or $1,000 if you use specific MoneyLion products.

- Invest in stocks and crypto: MoneyLion allows users to buy stocks and crypto. Some cash advance apps that double as mobile banking solutions let you buy stocks. Only a few of them also let you buy crypto.

- Build your credit: MoneyLion’s cash advance does not impact your credit. The fintech company does not check your credit for this product. However, you can take out a credit builder loan through MoneyLion and use Instacash to repay it. If you get a credit builder loan, your maximum cash advance goes up to $700. Repaying the credit builder loan with Instacash will improve your credit score.

Cons

- You might have to pay the turbo fee: MoneyLion doesn’t require users to get an instant transfer. However, it can take up to five days for the cash to arrive in an external bank account if you opt for the free transfer. If you can wait a week, you are fine and can do the free transfer. However, if you are transferring funds to an external account and need them within three days, the free route doesn’t guarantee they will arrive on time.

- You can borrow more money through alternatives: This common problem plagues many cash advance apps. You can borrow more money with a credit card or personal loan. Granted, you don’t need the best credit score to get a cash advance, and you can access up to $1,000 if you use RoarMoney. MoneyLion is better than most cash advance apps, but it may not be for you if you have to borrow over $1,000.

- You start with a low cash advance limit: While a $500 cash advance can help with expenses, you don’t start with that number. It can take several months to qualify for the highest cash advance available. MoneyLion may not be the best choice for people who need money right now and don’t have enough time to build up their cash advance limit.

Employer-Sponsored Apps Like Albert

Some cash advance apps work with employers to let workers access money early. These earned wage access apps entitle you to a percentage of every paycheck a little early. Many of these apps charge a small fee for each transfer but typically waive that fee if you can wait a few days before receiving funds.

PayActiv: Best for Saving Money

PayActiv is an earned wage access app that lets over two million employees access a portion of their paychecks early. PayActiv waives its small fee for some types of money transfers and has several discounts available through its partners. You can find exclusive discounts for various products and services by downloading the PayActiv app.

Highlights

Pros

- You don’t have to worry about repayment: PayActiv uses your payday to repay the cash advance. This process happens automatically.

- Avoid payday loans and overdraft fees: PayActiv is a viable alternative that can shield you from excessive fees and predatory financial products.

- Goal-based savings accounts: You can create multiple accounts and distribute your paycheck across each one. You can create goal-based savings accounts for a vacation, down payment, retirement, and other goals.

Cons

- Low cash advance: You can only borrow up to $200 with PayActiv, which is lower than some of the other cash advance apps on this list.

- Your employer has to use PayActiv: Your employer needs to use PayActiv for you to receive a cash advance. Other apps are more convenient.

- The limit does not refresh until the next pay period: If your employer pays you once every two weeks, you have to wait two weeks before taking out a $200 cash advance from your earned wages.

DailyPay: Best for High Cash Advance

DailyPay is an earned wage access app that lets you access all of your paycheck early. Your cash advance depends on how much you earn and can be higher than any other option. Your employer needs to use DailyPay to be eligible for cash advances. The app integrates with various payroll software and works smoothly in the background.

Highlights

Pros

- High cash advance: You can get your entire paycheck early instead of waiting for payday.

- Daily cash advances: You can request money from DailyPay every day as your earned wages get updated.

- Save money from payday loans and overdraft fees: You won’t have to incur high fees or take on risky loans to cover an emergency expense.

Cons

- You cannot avoid the fee: Waiting 1-3 business days will reduce the fee, but there is no option for a fee-free transfer.

- Cyber attacks: DailyPay is an online app that has access to your paycheck. This can be perfectly fine, but if a hacker infiltrates the system, your earnings could be at risk.

- DailyPay can lead to bad financial habits: The EWA app works well if you use it to cover emergency expenses. However, fees can add up quickly if you use the app for every purchase and rack up debt. This risk is present for every cash advance app, but it’s more important to keep this in mind for DailyPay since it has one of the most generous cash advance policies.

Peer-to-Peer Apps

Peer-to-peer lending apps can be a great way to borrow money. The fundraising potential from P2P apps usually exceeds cash advance and earned wage access apps. Some P2P apps let you set an interest rate so you don’t overpay. These apps tend to run credit checks to ensure you are in a good position to repay other members’ contributions.

SoLo Funds

SoLo Funds is a P2P platform that embraces community finances. Members support each other financially. Borrowers can get anywhere from $20-$575, while lenders receive a tip which is similar to interest on traditional loans. Borrowers can decide on the tip amount, but a higher tip will make it easier to get capital.

Highlights

Pros

- SoLo Funds only runs a soft credit check: Many lenders run hard credit checks during the application process. A hard credit pull will hurt your credit score, but SoLo Funds only runs a soft credit check. A soft check does not hurt your score.

- You get to decide the tip: Most lenders tell you what the interest rate will be, but SoLo Funds lets you set a rate instead. You can end up getting cash at a lower interest rate than average.

- Become a part of the community: SoLo Funds can become a reliable stop for funding. Once you understand how SoLo Funds works as a borrower, you can consider joining as a lender. SoLo Funds gives people the opportunity to receive funds and help people who need extra cash.

Cons

- You may have to set a higher tip: The tip cannot exceed 15% of the loan amount, but some people have to set higher tips to get capital. Investors may feel less inclined to give you money if you are new or have a low SoLo score. A higher tip can entice them to give you money, but it will cost you extra.

- Your loan goes to a debt collection agency after 90 days: This disadvantage isn’t an issue if you repay the loan within its 35 day term. However, if you fall behind, your debt can quickly go to a third-party collections agency. Other cash advance apps are more generous and automatically pull funds from your bank account to prevent this type of issue.

- Low cash advance amount: You can only borrow up to $575 with SoLo Funds, and it can be quite a hassle to get cash in the first place. You have to position your P2P loan request and compete with other borrowers who need money.

LendingClub

LendingClub connects borrowers with investors and has given capital to over 4 million borrowers. You can borrow up to $40,000 through a LendingClub personal loan. The company can help you with your financial needs, but it’s more than just a place to borrow money. LendingClub also has several checking and savings accounts and CDs with competitive rates.

Highlights

Pros

- Access up to $40,000: The high personal loan amount dwarfs what you can get from a cash advance app.

- Fixed monthly payments: You can adjust the loan’s term based on your budget, and fixed monthly payments provide stability. You won’t have to worry about your monthly payment increasing if rates go up.

- Receive loan offers in minutes: It doesn’t take long to submit your information and receive loan offers. LendingClub only runs a soft credit check when showing you the offers.

Cons

- Hard credit check: LendingClub runs a soft credit check when you ask for a quote. However, the company will conduct a hard credit check once you submit a loan application. A hard credit check will reduce your credit score by a few points.

- The interest rate can get high: Your interest rate is based on your credit score and other factors. While an excellent credit score can grant you a lower rate, consumers with bad credit can get stuck with a 36% APR.

- You have to fulfill the minimum credit score requirement: Borrowers need a 600 credit score or higher to qualify for financing. Other cash advance solutions do not have credit score requirements.

What To Look for in a Cash Advance App

Consumers can choose from many cash advance apps, but some are better than others. You should look for the following details when comparing cash advance apps:

- Maximum cash advance: A higher limit is more enticing. If you can only borrow $250, you may need an additional funding source for emergency expenses.

- Fees and interest: Many cash advance apps do not charge interest, but they do have fees. Some apps get sneaky and end up charging high interest rates under the guise of fees. It’s not “interest,” but it is very similar in some cases.

- Credit checks: Look for a cash advance app that does not run hard credit checks. Some apps may require hard credit checks but also offer higher amounts. It’s not worth a hard credit check if you’re only receiving a few hundred dollars.

- Other perks: Some cash advance apps also offer mobile banking solutions, products to build your credit, and investment portfolios. If an app’s purpose starts and ends with the cash advance, you may not be getting the full mobile banking experience.

Risks of Cash Advance Apps

Cash advance apps can help during emergency expenses, but the risks can pile up if cash advance apps turn into a habit. If you continue taking out cash advances, you can find yourself behind on retirement goals and constantly living paycheck to paycheck. Cash advances are temporary band-aids you can use for surprises, but relying on them can hurt your finances and result in costly fees.

FAQ

How fast do cash advance apps like Albert work?

Cash advance apps like Albert can give you funds instantly, while you can avoid a fee by waiting 1-5 business days.

How is Albert different from other cash advance apps?

Albert is different for its 0% APR and low fees. The app also lets you invest and build up your savings.

What apps let you borrow money instantly?

Apps like Albert, Cleo, Dave, and MoneyLion let you borrow money instantly.

What happens if you don't pay Albert back?

If you do not pay Albert back, the company can automatically use funds from your next paycheck to replenish the cash advance.

How do cash advance apps work?

Cash advance apps connect with your bank account and give you extra funds right away or within a few days. These apps use your next paycheck to repay the cash advance.

Are apps like Albert better than payday loans?

Apps like Albert can help you save a lot of money and avoid high interest rates. They tend to cost less than traditional payday loans.

How quickly can I get my cash advance?

You can get a cash advance instantly for a small fee. If you can wait a few business days, you can avoid the fee or end up with a smaller fee.

Will apps like Albert help me build credit?

Apps like Albert typically do not help with credit building. Some apps offer secured credit cards and other products that build your score. However, paying back a cash advance on time will not impact your score.